On 5 June 1933, the United States went off the gold standard, a monetary system in which currency is backed by gold, when Congress enacted a joint resolution nullifying the right of creditors to demand payment in gold. The United States had been on a gold standard since 1879, except for an embargo on gold exports during World War One, but bank failures during the Great Depression of the 1930s frightened the public into hoarding gold, making the policy untenable.

Soon after taking office in March 1933, Franklin Delano Roosevelt declared a nationwide bank moratorium in order to prevent a run on the banks by consumers lacking confidence in the economy. He also forbade banks to pay out gold or to export it. According to Keynesian economic theory, one of the best ways to fight off an economic downturn is to inflate the money supply, and increasing the amount of gold held by the Federal Reserve would in turn increase its power to inflate the money supply. Facing similar pressures, Britain had dropped the gold standard in 1931, and Roosevelt had taken note.

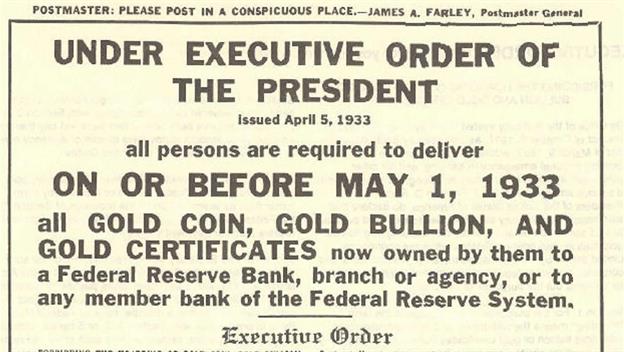

On 5 April 1933, Roosevelt ordered all gold coins and gold certificates in denominations of more than a hundred dollars turned in for other money. It required all persons to deliver all gold coin, gold bullion, and gold certificates owned by them to the Federal Reserve by 1 May for the set price of $20.67 per ounce. By 10 May, the government had taken in three hundred million dollars of gold coin and five hundred million dollars of gold certificates. Two months later, a joint resolution of Congress abrogated the gold clauses in many public and private obligations that required the debtor to repay the creditor in gold dollars of the same weight and fineness as those borrowed. In 1934, the government price of gold was increased to $35 per ounce, effectively increasing the gold on the Federal Reserve’s balance sheets by 69 percent. This increase in assets allowed the Federal Reserve to further inflate the money supply.

The government held the $35 per ounce price until 15 August 1971, when President Richard Nixon announced that the United States would no longer convert dollars to gold at a fixed value, thus completely abandoning the gold standard. In 1974, President Gerald Ford signed legislation that permitted Americans to again own gold bullion.

Rico says it was a mistake, not fixed until 1974...

-----Original Message-----

From: "HISTORY | This Day In History" <tdih@emails.history.com>

Sent: Monday, 5 June, 2017 06:00

To: "mseymour@proofmark.com" <mseymour@proofmark.com>

Subject: 1933: FDR takes United States off gold standard

| Jun

5 | THIS DAY IN HISTORY |

|

| 1933 |

| FDR takes United States off gold standard |

|

| On June 5, 1933, the United States went off the gold standard, a monetary system in which currency is backed by gold, when Congress enacted a joint resolution nullifying the right of creditors to demand payment in gold. The United States had been on a gold standard since 1879, except for an embargo... read more » |

|

No comments:

Post a Comment